Trump Should Finish What He Started

A guestpost calling for Trump to finish radically reforming the tax system

Introduction

On June 24, 2016, the Republicans introduced “A Better Way,” a blueprint for tax reform billed as the most significant overhaul of the U.S. tax system since the income tax first appeared in 1913. Positioned as a successor to the transformative reforms of 1986, the plan aimed to fundamentally reshape how taxes are collected and how they influence economic decisions. For some, it was an idealistic endeavor, and for others, it was simply “another GOP tax cut.” But for those of us who spend way too much time immersed in public finance and tax policy, it felt inevitable. It was the logical next step in a long-evolving narrative. At the heart of the blueprint was the Destination-Based Cash Flow Tax (DBCFT), a model born from years of academic work and championed by economists like David Bradford, Alan Auerbach, and Jim Hines. The DBCFT represents a synthesis of decades-long debates on optimal taxation, incorporating principles designed to raise substantial revenue to finance what the government deems worthy without throwing wrenches into business decisions.

What's more, the ideas underlying the DBCFT weren't entirely new to U.S. policy circles. Back in 2005, the President's Advisory Panel on Federal Tax Reform, established by President George W. Bush, rolled out proposals that echoed the principles underlying the DBCFT. Their plans included lowering marginal tax rates, eliminating certain deductions, and promoting saving and investment—concepts that resonate with the DBCFT framework. Interestingly, aspects of this tax reform have found nods of approval from both sides of the political aisle. Jason Furman, who served as Chair of the Council of Economic Advisers under President Obama, has highlighted the merits of specific components, particularly those that promote simplicity in the tax code and encourage economic growth. In fact, many Democratic lawmakers and advisors, whether openly or in quieter conversations, have also recognized the value of this approach, underscoring their bipartisan appeal. The Tax Cuts and Jobs Act (TCJA) of 2017, the eventual enacted policy born out of “A Better Way” and signed by President Donald Trump, included provisions that have been recognized for their positive impact and could serve as common ground for future bipartisan tax policies. It’s true, parts of the TCJA genuinely are worth hanging onto.

When you peel back the layers, the tax reform plan put forth by the Republicans that was later embodied in the TCJA isn't so much a radical leap into the unknown as it is the culmination of a long journey through scholarly research and policy evolution. It reflects a convergence of ideas from economists, policymakers, and bipartisan commissions, all wrestling with the never-ending challenge of designing a tax system that promotes efficiency, fairness, and growth. In an era where the United States faces increasing competition from countries like China, mounting national debt, and the challenges of profit shifting by multinational corporations, the urgency of effective tax reform is undeniable. A tax system that enhances international competitiveness, supports long-term wage growth for workers, and simplifies the complex web of current tax regulations is essential, and the DBCFT offers a compelling framework to address these issues.

Advocacy for a Destination-Based Cash Flow Tax is really advocacy for consumption taxation in disguise, so it makes sense to first actually address what consumption taxes are, or, more importantly, what people mistakenly think they are (spoiler: they’re not just taxes on your latte habit.)

Consumption Taxation

Misconceptions about expert proposals are a common occurrence when implicit knowledge is required to understand academic writing, knowledge the general public may lack. This is particularly true in economics, a discipline inextricably linked to politics despite many academics' reluctance to engage with it. The definitions and mechanisms economists use to explain tax systems often bear little resemblance to the tax systems people actually encounter. An 'income tax' or 'wealth tax' in an optimal tax model can differ significantly from what people envision when they hear these terms or what politicians propose. When people hear "consumption tax," two common perceptions emerge:

It's what they pay at the store, a tax on purchases.

It's regressive, the tax burden falls more heavily on lower incomes.

The first is technically correct but definitionally imprecise. The second can be true but isn't a universal feature of consumption taxes. The key characteristic that defines a consumption tax is its intertemporal neutrality with respect to consumption choices, with intertemporal neutrality meaning that it treats present and future consumption equally and ensures that tax considerations do not distort the timing of consumption by individuals and businesses.

When you, an individual, receive money, you face two choices: to consume, or to save. This fundamental relationship was formalized by Robert Haig and Henry Simons, who proposed defining income according to its uses. The Haigs-Simons definition of income states that an individual’s income, Y, in any period equals their consumption, C, plus their change in savings, or, their net worth. A simple derivation yields that consumption is simply income minus any changes in savings. Formally:

Y = C + ΔS → C = Y - ΔS

This relationship reveals that we can measure consumption just by tracking money coming in, your income, and money going into savings. This is called a cash-flow approach: you start with all your income (salary, investment gains, etc.), subtract what you save, and what's left is what you consumed. Under our current income tax system, figuring out taxable income is incredibly complex. We need rules for when to count income (realization), how to track the original cost of assets (basis), how to spread out the cost of long-term investments (depreciation), when to count future income (accrual), and how businesses should track their goods (inventories). All these complications exist because we're trying to measure and tax income itself. But if we switch to taxing consumption through a cash-flow system, we can throw all these complex rules away. We don't need them anymore because we're not trying to precisely measure income - we just need to track money flowing in and out of savings. Fundamentally, a consumption tax is simply one that does not penalize savings.

This broad yet precise definition of consumption taxation helps clarify why the common perceptions mentioned earlier are incomplete. While a sales tax is indeed a consumption tax, a simple payroll tax, when purely levied on wage income, is economically equivalent to a consumption tax. Another seemingly identical relationship emerges if you were to uncap 401ks: allowing individuals to put unlimited amounts into their 401k to withdraw at their discretion effectively converts our income tax system into one that taxes consumption. Let's explore this equivalence through an example. Imagine a software engineer earning $400,000 annually who plans to save aggressively. She intends to save 45% of her pre-tax income, and let's assume her investments triple over 20 years. Let's compare two systems that appear different but are mathematically identical:

Simple Wage Tax (35%): She pays tax immediately on her $400,000 salary, leaving $260,000. She saves 45% ($117,000) and spends $143,000 on current consumption. After 20 years, her savings triple to $351,000, all available for future consumption with no additional taxes.

Uncapped 401k System (35%): She first sets aside $180,000 (45% of $400,000) in her 401k pre-tax. She pays 35% tax on the remaining $220,000, leaving $143,000 for current consumption. After 20 years, her $180,000 investment triples to $540,000. When withdrawn from the 401k, she pays 35% tax, leaving $351,000 for future consumption.

Notice how both approaches yield identical consumption in both periods ($143,000 now, $351,000 later). The wage tax system appears to ignore gains entirely, while the 401k system seems to tax them at the same rate as ordinary income. Yet they produce exactly the same outcome in terms of consumption, these are simply different ways of implementing a consumption tax. And of course, if we are simply modifying the treatment of savings in our current income tax system through say, unlimited 401k-style accounts, we naturally maintain its progressive structure, dispelling the notion that consumption taxes must be regressive.

The Work-Leisure Tradeoff

All taxes in our feasible toolset are going to introduce some level of economic distortion, but the extent of said distortion depends heavily on tax design. Both income and consumption taxes influence the trade-off between work and leisure. We work to consume, not to accumulate pieces of paper with numbers on them. Every hour spent working means giving up an hour of leisure, whether it’s lounging on the couch or binge-watching a TV show. Now, imagine you earn $300 an hour and face a tax rate of 33%. Whether it’s an income tax or a consumption tax, you’re left with $200 to spend. The core distortion, the reduced reward for working an additional hour, remains the same under both systems; the initial choice between work and leisure is equally affected.

Let’s put some structure around this work-leisure trade-off with a simple model. Consider L to be leisure, w to be the wage rate and t is, of course, the tax rate. When you choose to work for an hour instead of enjoying your free time, you forgo the utility or satisfaction that hour of leisure could have provided. In return, you earn wages, but those wages are, of course, reduced by taxes. The amount you have available to spend is:

(1-t)w

This represents your after-tax earnings per hour of work, which directly translates into your ability to consume. To put it another way, every hour of leisure foregone is compensated by this amount of consumption power. The math is simple: just plug in the numbers from before! If your hourly wage is $300 an hour, and the tax rate is 33%, your after-tax earnings are (1-t)w, or $200 dollars! Every hour of leisure foregone translates into $200 worth of consumption power; your take-home pay quantifies what you exchange for sacrificing an hour of leisure. The higher your wage or the lower the tax rate, the more consumption you can achieve by giving up leisure.

This might seem repetitive, but I really want to hammer down this time-neutral consumption point, especially within the context of work incentives. So far, we've focused on how taxes affect immediate consumption power, but what happens when you choose to save that $200 instead of spending it right away? When you defer your consumption, you let your money grow at an interest rate, r. Here’s how this would look under the two tax regimes:

Income Tax: Your earnings are taxed both when you work and when your savings generate returns. Thus, if you save and let your earnings grow, the future consumption per hour of foregone leisure becomes:

(1-t)w*[1+(1-t)r]^n

The only takeaway from this expression that matters is that your (1-t)w term applies twice: first to your wages, and then to your investment returns, reducing the growth of savings over time. Also, n are years.

Consumption Tax: Your wages are only taxed once (note that it technically doesn’t matter when, remember our uncapped IRA and payroll tax stuff! The underlying point is about neutrality between present and future consumption) The return on your savings is untouched, allowing them to grow fully until you spend them. The future consumption per hour of foregone leisure is:

(1-t)w*[1+r]^n

Here, the tax system preserves the full growth of your savings, maintaining neutrality between present and future consumption.

By characterizing (1-t)w as leisure foregone, we see it represents the immediate reward for giving up leisure in terms of consumption power. This reward can either be consumed immediately or saved for future consumption. Both tax systems introduce an initial wedge between work and leisure, as reflected in the no-tax benchmark of w[1+r]^n. However, their paths diverge when savings enter the picture. Under a consumption tax, investment returns grow unimpeded—the timing of taxation doesn't matter, as your consumption power is taxed only once, regardless of when you choose to spend it. In contrast, an income tax creates a second barrier by taxing investment returns, causing a compounding erosion of future consumption power over time.

Why Should We Care?

As explained earlier, the fundamental economic advantage of consumption taxation over income taxation lies in its treatment of intertemporal choices. But why does this matter? The answer lies in how economists understand the relationship between savings and economic growth. When individuals save rather than consume immediately, these savings don't simply disappear from the economy—they are transformed into productive investment.

Whether through bank deposits that become business loans, direct stock market investments, or real estate, savings flow into capital formation. This new capital takes many forms, each driving economic growth through different channels. Physical capital like factory machinery and equipment makes workers more productive by increasing the capital per worker. But savings also fund technological innovation through research and development, leading to better production methods and entirely new products. They finance human capital formation through education and training, improving worker skills and knowledge. This process of capital accumulation is central to how economies grow. While it might seem intuitive that more consumption always benefits the economy, the reality is more nuanced. In the short run, increased consumption can boost GDP through higher aggregate demand (I don’t actually believe this in normal times, since the Federal Reserve would engage in monetary offset, but whatever, I’m making a point). However, long-run economic growth isn't determined by how much we consume or by aggregate demand more broadly. Rather, it's constrained by our economy's productive capacity—what economists call long-run aggregate supply. Simply consuming more doesn't expand this capacity. What does expand it is saving and investment in new capital formation, which increases what our economy can produce in the future.

Consider an investment opportunity yielding a 15% return. With a $200 investment generating $30, an investor facing a 35% corporate tax followed by a 45% personal income tax would see their return reduced from $30 to just $11.70. This tax wedge between gross and net returns can make otherwise productive investments unprofitable, reducing capital formation and ultimately leading to lower output, employment, and wages. In contrast, under a consumption tax system—even with a high rate—the relative return on investment remains unchanged. If a 50% consumption tax means $200 can buy $100 of goods today, and the full $30 return can buy $15 of goods in the future, the effective rate of return remains 15%. The consumption tax preserves the incentive to invest in productive capital formation, which is crucial for long-run economic growth.

Growth Is Good.

I mean, yeah. Growth is good.

While this may seem like a simplistic statement, the evidence for economic growth's broad positive impact on human welfare is compelling. Higher GDP per capita isn't just about material consumption—it correlates strongly with improvements across numerous dimensions of human wellbeing. From increased life expectancy and reduced child mortality to better environmental quality and even stronger social cohesion through higher interpersonal trust, economic growth underpins societal progress. Rising living standards provide families with improved access to healthcare, better educational opportunities, and more leisure time for personal pursuits and family connections. Given growth's importance, we must carefully consider how tax policy affects economic incentives. Research consistently shows that tax structures significantly influence both work and investment decisions. Tax policies obviously affect growth, ergo alleviating the biases in the tax code that work against growth through using consumption taxes as the main and potentially most efficient revenue raiser should be a no-brainer.1

Tax Simplicity

Beyond growth incentives, consumption taxation offers a powerful yet underappreciated advantage: administrative simplicity. Consumption is inherently more observable and measurable than income, which requires tracking complex changes in wealth over time. Our current income tax system is burdened with unavoidable complexities. To measure income accurately, we need elaborate rules for everything from when to count gains to how to spread investment costs over time. Consider a business owner trying to determine their taxable income: they must navigate when to recognize revenue, how to depreciate equipment, track inventory costs, and distinguish between immediate expenses and capital investments.

David Bradford once pointed out that these challenges have long been acknowledged, even by the U.S. Supreme Court. In 1933, Justice Benjamin Cardozo, writing for the Court in Welch v. Helvering, captured the difficulty of distinguishing between capital expenditures and current business expenses. “One struggles in vain for any verbal formula that will supply a ready touchstone," he wrote. "The standard set up by the statute is not a rule of law; it is rather a way of life. Life in all its fullness must supply the answer to the riddle.” Bradford emphasized that such complexities are inherent in income taxation. In contrast, consumption taxes sidestep these issues entirely through immediate expensing of all business expenditures–no need to seek guidance from 'life in all its fullness' when every purchase is treated the same way.

A consumption tax, measured through cash flows, sweeps away these complexities. We simply track money coming in and money going to savings–the difference is consumption. No more puzzling over depreciation schedules or inventory accounting. No more artificial distinctions between types of business expenses. While any tax system in a complex economy requires some administration, consumption taxation removes these fundamental complications without introducing significant new ones. The simplicity stems from measuring what people actually do with their money rather than trying to calculate theoretical concepts of income. This emphasis on real cash flows rather than theoretical accounting concepts naturally leads us to the Destination-Based Cash Flow Tax–a practical implementation of these principles. Now that we understand what a consumption tax is and why economists favor them–both for their growth effects and administrative simplicity–we can better appreciate the blueprint behind the Tax Cuts and Jobs Act. While often portrayed as "just a tax cut," it represented an ambitious attempt to reshape the U.S. tax system toward consumption taxation, drawing on decades of optimal tax research, addressing global profit shifting concerns, and incorporating modern thinking about compliance costs. Though only partially successful, it marked a significant step in this direction.

#DBCFT

We can operationalize a Destination Based Cash Flow Tax (DBCFT) as follows:

Full expensing, an immediate deduction of all capital investments.

Elimination of interest deductibility for non-financial businesses.

Border adjustments through import taxation and export exemption.

These components work together to create a comprehensive approach to business taxation, grounded in consumption tax principles, that addresses both domestic and international corporate incentives. I'll explain what each component entails and the connection to consumption taxation should become clear throughout, but I'll highlight these links where particularly relevant.

Full Expensing

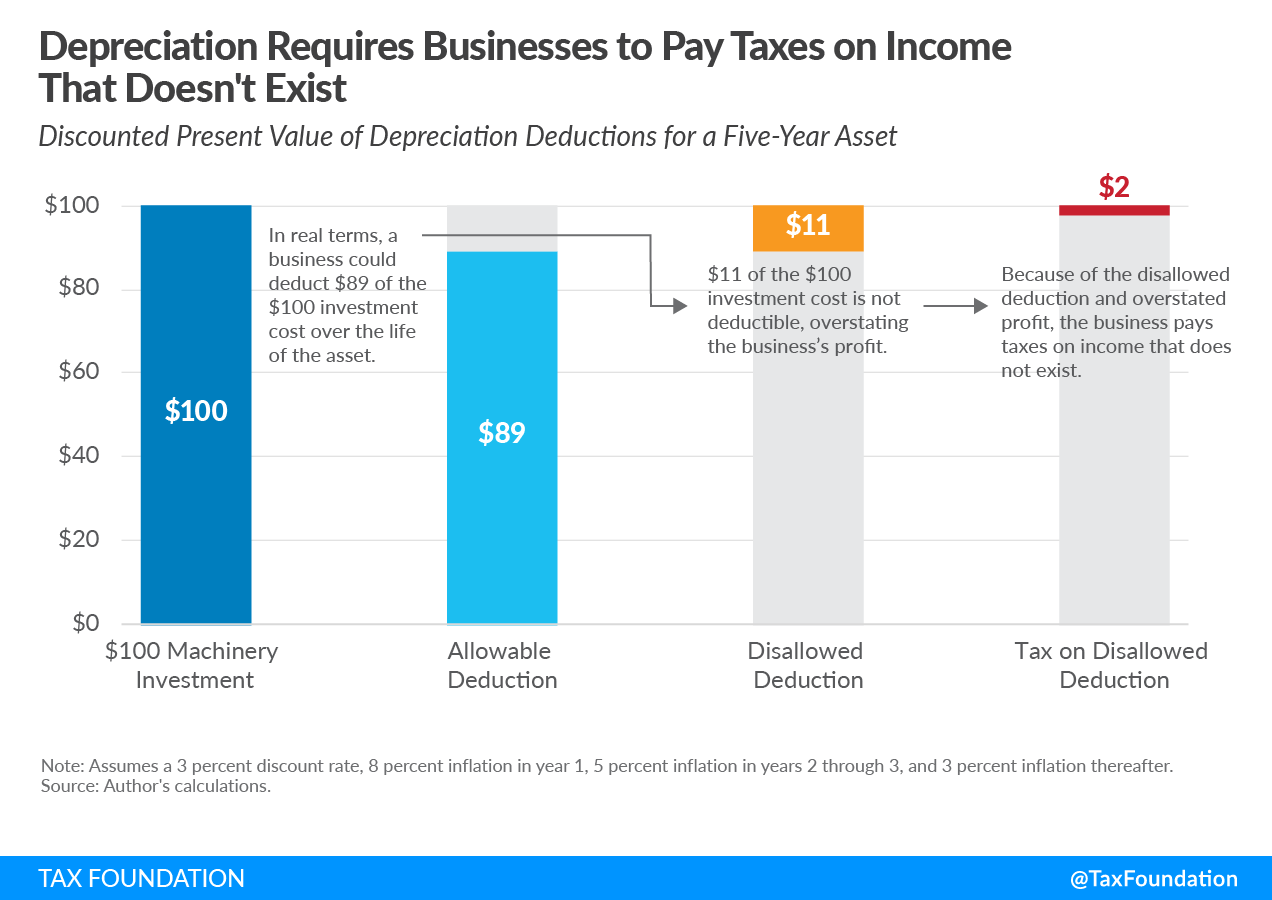

Profits are calculated as revenue minus costs. The corporate income tax is a tax on corporate profits. Hence, when a corporation calculates their income to report on a 1120 form, they take their revenue and subtract away their costs, mostly. As it turns out, you’re not actually allowed to subtract away all your costs in the year they’re made. More specifically, and unfortunately, corporations typically can't deduct the full cost of their capital investments in the year they make them. When said costs are incurred, they are only permitted to deduct them over several years based on preset depreciation schedules.

Imagine you own a small bakery. Your old commercial oven is aging, and you decide to invest in a new industrial-grade oven system for $800,000 to increase production capacity. Despite writing that check today, you can't deduct the full $800,000 from this year's taxes. Instead, under the Modified Accelerated Cost Recovery System (MACRS), this equipment is classified as a 5-year property, and you'll need to spread the deductions over several years according to a preset schedule. This system exists because traditional accounting principles view capital investments differently from regular business expenses like wages or ingredients. The idea is that since the oven will generate value over many years, its cost should be spread out over its useful life. So while you can immediately deduct the cost of flour or your employees' wages, major equipment purchases must be "depreciated".

If you're the kind of person who picks up on things straight from the charts, here's a great visualization. I'll follow it up with a more concrete example to make it more intuitive.

Let's say in the first year your bakery can deduct 20% of the cost, then 32% in year two, 19.2% in year three, and smaller amounts in the fourth and fifth years (with a small remainder in year six). So even though you're out $800,000 for your new oven today, you'll only get to claim $160,000 in deductions this year ($800,000*20%), $256,000 next year ($800,000*32%), and smaller amounts in following years. When you account for the time value of money (a dollar today is worth more than a dollar tomorrow) and inflation, these spread-out deductions are worth significantly less than an immediate $800,000 deduction would be. Your bakery is not allowed a full, immediate deduction for its investment costs, and thus, the tax code overstates your profit, which leads to a higher tax burden and raises your cost of capital.

Think about what happens when you invest in that new oven. For this investment to make sense, it needs to at least break even–providing enough return to cover your costs, compensate for inflation, and make up for having your money tied up instead of available for other uses. This basic break-even amount is what economists call the normal return to investment. But successful businesses often earn more than just this normal return—:they might develop a popular new product, build a strong brand name, or find an innovative way to cut costs. These extra returns above the normal break-even amount are called supernormal returns. The current tax system, by delaying deductions for capital investments, effectively taxes the normal return to investment, creating a bias against saving that doesn't exist with full expensing. When your bakery has to spread deductions for the oven over many years instead of claiming them immediately, the tax code is effectively placing a higher burden on future versus present consumption:

Remember our earlier discussion of consumption taxes? Their key advantage is treating present and future consumption neutrally. We can achieve this same neutrality in the corporate tax system by allowing full expensing—immediate deduction of investment costs—which effectively exempts the normal return from tax.

But how do we measure whether a tax system is neutral toward investment decisions? Economists use two key measures. The marginal effective tax rate (METR) reflects how taxation increases the cost of capital at the break-even point of an investment—that is, how taxes affect decisions about the scale of investment projects. The average effective tax rate (AETR), on the other hand, measures the average tax cost for a hypothetically profitable investment over its entire life, which influences decisions about where to locate discrete investments.

We can formalize how the tax treatment affects business decisions. Your bakery, when deciding whether to buy that $800,000 oven, needs to earn enough return to cover not just the cost of equipment, but also

The opportunity cost of having money tied up instead of invested elsewhere, the discount rate.

The physical wear and tear, the depreciation.

The tax implications of the investment.

Hall-Jorgensen captures these factors using a quite elegant formula that shows exactly how much pre-tax return a business needs to justify an investment—a formula that has become the foundation for how academics analyze investment decisions with respect to tax policy:

c = q(r+δ)[(1-k)(1-uz)/(1-u)]

Here, c represents the minimum return needed to make an investment worthwhile, the cost of capital. The first part, q(r+δ), shows the basic economics without taxes: q is the price of the investment, our $800,000 oven, r is the discount rate, the cost of having money tied up, and δ, represents depreciation, how quickly the oven wears out. The second part, [(1-k)(1-uz)/(1-u)], shows how taxes affect the decision. Here, k represents any investment tax credits, u is the tax rate, and z is the present value of depreciation deductions. Under our current system, where deductions are spread out over many years, z is less than 1 because future deductions are worth less than immediate ones, i.e., our bakery only gets to deduct a portion of the oven’s cost each year. For instance, here are the present values of depreciation deductions for manufacturing sectors, where all values are less than one. These graphs are based on estimates from Zwick and Mahon, as presented in Curtis et al. , using IRS sector-level depreciation data.

What happens if we allow full expensing, the ability to deduct the entire cost of capital in the year it's incurred, making z equal to 1? Let’s see the algebra!

c = q(r+δ)[(1-k)(1-u)/(1-u)], so the tax rate terms cancel out and,

c = q(r+δ)(1-k)

Notice that the tax rate, u, completely disappears from the equation. Under full expensing, taxes no longer affect whether an investment is worth making: the bakery owner can make the same decision they would in a world without taxes. In technical terms, the marginal effective tax rate on new investment falls to zero. Remember our earlier discussion of consumption taxes. Their key feature is equal treatment of present and future consumption. Full expensing achieves this same property in the corporate tax system. When a business can immediately deduct the full cost of investments, the tax system no longer creates a bias against saving and investment. This eliminates the bias against the normal return on investment—the minimum return needed to make the investment worthwhile—while still allowing the government to tax above-normal returns.

However, eliminating the bias against the normal return is only part of the story. While full expensing ensures neutrality for investments yielding a normal return, it doesn't address how to tax supernormal returns, profits that exceed the break-even point. Traditionally, economists viewed these excess returns as rents that could be taxed away with minimal economic distortions. This included pure economic rents from unique advantages like prime land locations or natural monopolies, but also other forms of above-normal returns. The logic was straightforward: since these returns exceeded what was necessary to incentivize investment, taxing them wouldn't alter business decisions. But this view is too simplistic for two reasons. First, what appears to be an economic rent often reflects compensation for risk-taking and innovation that is necessary to incentivize investment. Second, traditional models assumed closed economies where capital couldn't move across borders. In today's global economy, high taxes on supernormal returns can drive businesses to shift their profitable activities, especially mobile assets like intellectual property, to lower-tax jurisdictions. They might even reincorporate entirely through inversions, changing their tax residence while maintaining their economic operations.

A pharmaceutical company that successfully brings a new drug to market often appears to earn extraordinary profits during the patent’s life. These profits might suggest monopoly-like rents due to the temporary exclusivity provided by intellectual property laws. But looking deeper, these returns are often necessary to offset the immense costs of R&D, clinical trials, and navigating a decade-long regulatory process—costs that are only recovered if the drug succeeds. Many candidates fail at different stages of development, making those outsized profits a critical counterbalance to the high risks inherent in the industry. Similarly, a tech company that develops a transformative product might earn extraordinary profits for a few years. These profits aren’t guaranteed either, a few successful projects make up for numerous failures along the way.

In these cases, high rates of taxation on supernormal returns can create unintended consequences. While it might seem efficient to tax excess profits (well, it is relatively more efficient, you can’t just jack up the rate to say, 55% with no consequences, especially since you have to think of the U.S. as a competitor in the global system of tax regimes), this approach risks discouraging the investments necessary for innovation, as it diminishes the rewards for risk-taking. In more “economic” terms: Despite full expensing not distorting investment decisions on the intensive margin, the average tax rate is still important as it highly influences the extensive margin, the decision on where to set up shop in the first place. For a company deciding where to establish an R&D facility or house its intellectual property, the overall tax burden, including taxes on profits, heavily influences the choice. Countries with lower ATRs can attract these mobile activities, while higher ATRs risk driving them away.

Disentangling the source of supernormal returns turns out to not be easy. (This shows up in the literature under various terms like “supernormal returns,” “inframarginal returns,” and “quasi-rents.” Sometimes they mean slightly different things depending on how the author frames it, but you’re usually working in the same ballpark.) Optimal tax rates tend to vary over time, and trying to constantly update policy is idiotic. Still, breaking down supernormal returns could give a rough idea of the kind of rates a country might aim for. Set tax rates too high on supernormal returns, and you risk discouraging domestic investment and driving mobile, high-value activities abroad. Set them too low, and you miss out on revenue from rents that could be taxed efficiently without messing up behavior. The challenge is dealing with the uncertainty of figuring out where these returns come from while balancing tax policy, firm decisions, and the facts of global competition.

A tax on cash flow, enabled by full expensing, remains the better policy direction. By shifting focus to consumption rather than income, it eliminates distortions and achieves time-neutrality for investments by exempting the normal return. Full expensing allows businesses to recover costs immediately, which encourages capital formation and aligns incentives with long-term growth. In this framework, the government effectively becomes a silent partner in enterprise, sharing both investment costs and returns. This neutrality lets firms scale projects without altering their opportunity set, while also capturing a share of supernormal return. This approach, by keeping things simple and aligned with economic incentives, makes cash flow taxation a no-brainer for modern economies.

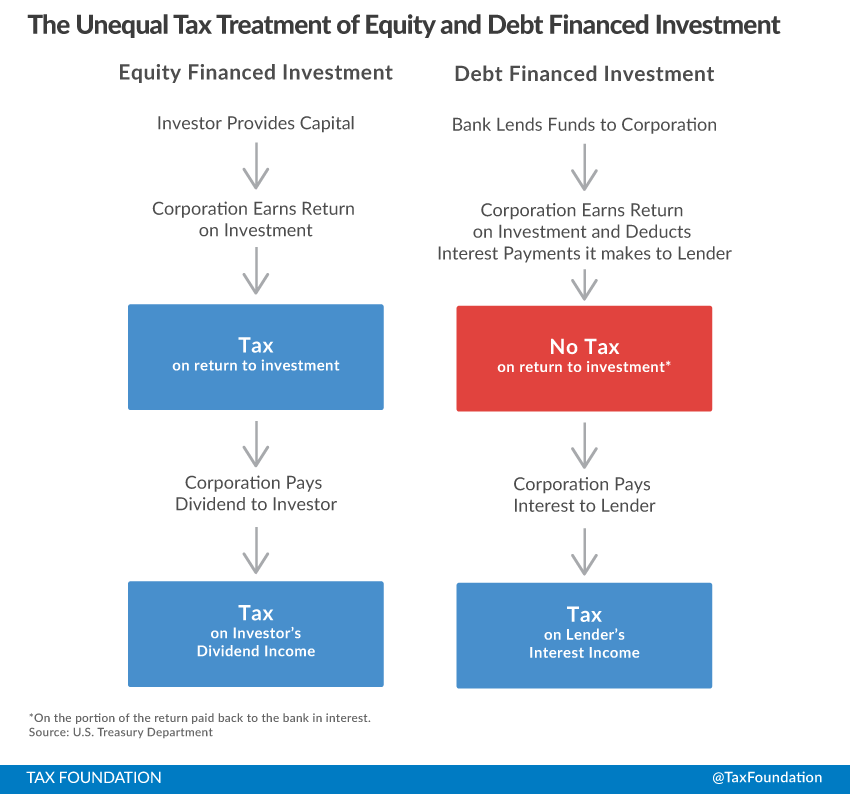

The Treatment of Debt and Equity Financing

Imagine you’re starting a small coffee shop. You’ve found a great location and plan to expand into catering, but you need $200,000 to get started. How do you raise the money?

One option is to take out a loan. You borrow the money from the bank and agree to pay it back over time with interest. This is debt financing. The advantage is you retain full ownership of your coffee shop, but you’re locked into regular payments, which can strain your finances during tough times. Another option is to bring on an investor. This is equity financing, where someone provides the money in exchange for part ownership of the business. You don’t have to worry about making loan payments, but your investor will take a share of the profits and likely have some say in how the business is run.

Both options have trade-offs, and most businesses use a mix of debt and equity to fund operations. What’s less obvious is how the tax code influences these decisions. The tax treatment of debt and equity isn’t neutral. Businesses can normally deduct interest payments on debt from their taxable income, making debt financing more attractive. In contrast, returns to equity, such as dividends or capital gains, are not deductible, making equity financing comparatively less appealing.

This unequal treatment nudges businesses toward borrowing more than they might otherwise. For some, this can mean taking on debt not just to fund operations but also to take advantage of the tax benefits. For example, restructuring a company’s balance sheet to replace equity with debt can lower a firm’s tax bill, benefiting shareholders but leaving taxpayers to pick up the slack. Over time, this preference for debt has raised concerns about financial stability. Firms heavily reliant on debt may find themselves more vulnerable during economic downturns, when revenues drop but fixed interest payments remain due. In international contexts, corporations often borrow in high-tax countries to maximize deductions, which can shift the financial burden and influence where profits are ultimately reported. This dynamic has drawn attention from policymakers and continues to play a role in discussions about global tax reform.

While the Tax Cuts and Jobs Act introduced a 30% limit on interest deductibility as part of its reform efforts, the way this limit is calculated has recently shifted. From 2018 to 2021, the limit was based on earnings before interest, taxes, depreciation, and amortization (EBITDA). Starting in 2022, however, the calculation tightened to earnings before interest and taxes (EBIT), dropping depreciation and amortization from the base. This change significantly reduced the allowable deductions for capital- and R&D-intensive businesses, increasing their effective tax burden. Combined with rising interest rates, this has exacerbated financial pressures for firms with high debt loads, subjecting more businesses to the interest limit.

While these limitations represent progress in addressing the debt-equity disparity, the fundamental bias persists. At its core, debt and equity both represent funding sources that businesses rely on to operate and grow. While they differ in their risk profiles and claims on a company’s resources, it’s unclear why the government should favor one over the other. Decisions about financing should reflect genuine market conditions and a company’s business needs, not distortions created by tax policy. A neutral tax code would let businesses choose the option that makes the most sense for them without unnecessary incentives or penalties.

Border Adjustment

At its core, a border adjustment in taxation refers to the application of taxes or exemptions when goods or services cross international borders. For the DBCFT, it operates on two key principles: imports are taxed and exports are relieved of taxation through rebates. To illustrate, imagine a company that manufactures furniture in the United States. Under a system with border adjustments, when this company sells its chairs to international buyers, the revenue it earns from those exports would be exempt from taxation. Conversely, if it imports fabric from another country to upholster those chairs, the value of the imported fabric would face taxation. These paired actions—taxing imports and exempting exports—ensure that goods are taxed based on where they are consumed rather than where they are produced. This shift in focus aligns with the broader economic principle of taxing domestic consumption.

An import tax increases the cost of foreign goods for domestic consumers and reduces demand for imports. As Americans purchase fewer imports, demand for foreign currencies declines, causing the U.S. dollar to appreciate. This stronger dollar, in turn, lowers the effective price of imports in dollar terms, partially offsetting the impact of the tax. On its own, while an import tax still reduces import volumes, the appreciation of the dollar mitigates this effect.

In contrast, an export rebate exempts exports from taxation, effectively reducing the price of U.S. goods abroad. This stimulates foreign demand for U.S. products, which increases the global demand for U.S. dollars, leading to dollar appreciation. However, as the dollar strengthens, U.S. goods become more expensive in foreign currency terms, offsetting some of the initial boost to export demand.

When import taxes and export rebates are applied together, they interact through the exchange rate. The import tax reduces demand for foreign currencies, while the export rebate increases demand for U.S. dollars. These forces reinforce each other, leading to a stronger dollar that neutralizes the effects of both adjustments. For example, if the export rebate lowers prices abroad by 20%, and the import tax raises prices domestically by 20%, the dollar’s appreciation cancels out these changes. As a result, trade flows, consumption patterns, and production decisions remain largely unaffected. The neutrality of border adjustments relies on symmetry; if the rates for import taxes and export rebates differ, or if adjustments are targeted toward specific goods or industries, distortions can arise. For example, favoring exports over imports could artificially bolster export-heavy sectors while disadvantaging others, disrupting the balance of economic incentives.

A potential complication emerges if some U.S. trading partners peg their currencies to the dollar rather than allowing exchange rates to adjust freely. Typically, countries peg their exchange rates to maintain the competitiveness of their domestic producers. In this scenario, pegging would still require allowing the dollar to appreciate to offset the effects of border adjustments, preserving neutrality. However, if a country resists appreciation and rigidly maintains its pegged rate, U.S. goods become more competitive in that market, giving U.S. exporters an unintended advantage. In essence, trading partners maintaining pegged exchange rates would, in effect, make the U.S. more competitive relative to their own economies.

While the economic mechanics of border adjustments are sound, their implementation faces institutional challenges, particularly regarding World Trade Organization (WTO) compliance. The WTO currently allows border adjustments for "indirect" taxes, such as value-added taxes (VATs) applied to goods and services, but restricts their use for "direct" taxes, like corporate or income taxes. While border adjustments under a DBCFT share many economic similarities with VAT systems, they also include deductions for domestic labor costs, which complicates their classification under existing WTO frameworks. Critics may argue that this treatment unfairly favors domestically produced goods over imports, since imported goods face the full border adjustment tax without a corresponding labor cost deduction.

Despite these concerns, many economists believe the distinction between direct and indirect taxes has little economic relevance, as both types of taxes can achieve similar outcomes. For example, replacing payroll taxes with a VAT at the same rate would be functionally identical to introducing a DBCFT, yet the former would align with WTO norms. Additionally, proponents of border adjustments argue that the goal of these policies is to tax domestic consumption, not domestic production. If implemented, the U.S. would need to prepare for potential challenges at the WTO, but I don’t think there’s really an issue here. Perhaps, this could be a source of unity where everyone across the political aisle can stick it to “globalism”.

Border adjustments align closely with the principles of territorial taxation. A territorial tax system, adopted by the U.S. in the TCJA, taxes companies only on profits earned domestically, excluding most foreign-earned income. For example, a U.S. company with a foreign subsidiary paying the foreign corporate tax would not owe additional U.S. tax on those profits when repatriated. In contrast, under the previous worldwide tax system, companies faced additional U.S. taxes on global earnings, discouraging repatriation and incentivizing profit shifting.

One of the most significant advantages of border adjustments is their ability to mitigate profit shifting by multinational corporations. Under the current international tax framework, companies often exploit differences in tax rates across jurisdictions through transfer pricing manipulation. For example, a U.S.-based parent company might sell products to its subsidiary in a low-tax country below market value, recording lower U.S. revenue while the subsidiary reports higher profits at lower tax rates, eroding the tax base in higher-tax countries. Similarly, by inflating import prices from these subsidiaries, companies can increase their deductible expenses in high-tax countries. This manipulation—which is often extremely hard to fix—costs governments billions in lost revenue and creates an uneven playing field between multinationals and smaller domestic businesses. Border adjustments effectively close these loopholes by tying taxation to the destination of goods and services rather than their origin. Under a border-adjusted system, manipulating export or import prices provides no tax advantage since the border adjustment would still apply to the transaction.

Furthermore, border adjustments eliminate the incentive to relocate production to low-tax jurisdictions. For instance, without border adjustments, a company producing goods in a foreign country could report profits in that jurisdiction to benefit from lower tax rates, even if those goods are sold primarily in the U.S. Under a border adjustment, however, the company would still face the same tax rate on U.S. sales, regardless of where the goods were produced. This levels the playing field, reducing the appeal of offshoring production purely for tax advantages.

Seriously, why is Ireland allowed to fund its healthcare and social programs with tax money that should be in the U.S., benefiting American taxpayers? American workers and families shouldn’t bear the cost of poorly designed and easily fixed tax policies. So I say, let the dollar appreciate and ensure American tax dollars support Americans!

Synthesis

Let's understand the DBCFT through the national income identity, or if you’re not interested in nerdy stuff, you can just skip to the Conclusion. When we talk about output, we're measuring everything produced in the economy. Some of this production is bought by domestic consumers (C), some is invested by businesses in things like equipment and buildings (I), some is purchased by the government (G), and some is sold abroad as exports (X). But we also need to subtract imports (M) because they're included in C, I, and G but weren't produced domestically:

GDP = C + I + G + X - M

A key relationship in international economics is that national saving net of investment equals net exports. This makes intuitive sense because if we're saving more than we're investing domestically, we must be investing the difference abroad, which requires running a trade surplus:

S - I = X - M

Private sector output generates income in two forms: returns to capital R, which includes profits, interest, and rents earned by businesses and investors; and returns to labor W, representing wages and salaries earned by workers. All this income is either spent on consumption or saved:

R + W = C + S

From these relationships we can show that private sector output equals:

R + W = C + I + X - M

And rearranging our saving-consumption relationship, we can show that consumption minus wages equals returns to capital net of saving:

R - S = C - W

Note the last equation, it shows that a tax on border-adjusted business cash flows (which taxes domestic sales C, allows deduction of wages W and investment I, and border adjusts by excluding exports X and taxing imports M) is equivalent to a tax on consumption net of wages. This equivalence reveals something I find beautiful about the DBCFT. It can be thought of as a value-added tax (VAT) combined with a deduction for wages–or equivalently, a VAT plus a wage subsidy at the same rate. Consider how a VAT works: it taxes domestic consumption by taxing all domestic sales and imports while ‘zero-rating’ exports–meaning exporters not only pay no tax on their export sales but also get refunds for VAT they paid on their inputs. But unlike a VAT, the DBCFT provides relief for labor costs through a wage deduction, which effectively works like a subsidy to wages at the tax rate. This means that while a VAT taxes all consumption, the DBCFT only taxes consumption financed from non-wage sources—mainly existing wealth (wealth accumulated before the reform that has already faced the income tax) and above-normal returns to investment.

Conclusion

This about sums up all you need to know about this stuff. There’s some other stuff, some counter-arguments I can anticipate and try and respond to, but this is a primer. There’s a funny tidbit at the end of the last section, that you can view a cash flow tax as a tax on “existing wealth.” Turns out, when you dip into “consumption tax world”, you find these sort of weird equivalences and similarities. Well, they’re not as weird to me, since many become ‘obvious’ (like the payroll tax) when working through our precise definition of consumption. But what’s actually important to note is that, technically, everything is a consumption tax. On the infinite time horizon, everything must be consumed eventually, right? Wealth is just the present value of all future consumption—yours, your heirs’, or whoever you donate it to. So a consumption tax is effectively a one-time tax on wealth, measured at its present value. (Real-world wealth taxes, by contrast, impose recurring levies, making them fundamentally different in how they hit deferred versus immediate consumption.)

The main point I’ve tried to convey is that a cash flow tax is good, and a destination-based cash flow tax is great. There’s something in here for everyone to like. If you’re an ardent progressive who believes big corporations wield enormous market power and extract rents through nefarious practices, then a tax on supernormal returns—or more accurately, pure profits—becomes immensely appealing. In fact, you could argue for higher statutory rates while still appealing to so-called "free market conservative" types, since this proposal doesn’t distort investment decisions at the margin. Sure, there’ll still be disagreements over the rate, but no good-faith free-marketeer like myself would deny that a 5% increase in the corporate tax rate combined with full expensing isn’t far more attractive than the status quo–especially considering current debt levels. There are various ways to finance the debt, but a key consideration is that the stability of government debt depends on the expected trajectory of tax revenue. At higher debt levels, optimization requires a tax base that minimizes the deadweight loss, or excess burden, of future tax increases. Given the established economic efficiency benefits of a DBCFT, it is evident that addressing U.S. debt and prospectively easing future bond market concerns should involve the use of consumption taxation. And everyone agrees that profit shifting and the erosion of the U.S. tax base is bad. For progressives, it’s the outrage of ‘how dare companies evade the IRS and pay a ‘zero corporate tax rate.’’ For conservatives, it’s the concern that ‘the erosion of corporate tax revenues incentivizes the government to raise my taxes!’ For protectionists, foreign buyers would still be subject to consumption taxes levied in their own countries. America could also mount a good fight against the World Trade Organization and win—they shouldn’t be able to push back against a stronger dollar!

The Tax Cuts and Jobs Act is set to expire soon. Some provisions have already started sunsetting, and Congress needs to figure out how to avoid a giant mess of tax hikes, revenue concerns, and threats to economic dynamism. Americans deserve a tax code that is simple, fiscally responsible, and growth-enhancing. While the TCJA’s scope goes far beyond this article , its original intent, as outlined here, should be remembered and championed as the foundation for future tax reform.

Especially if you want to make some Cowen-esque low social discount rate argument.

| A guest post by

|

Very interesting. I'm not certain I fully understand all of it and I'm even less sure I necessarily agree with all of it, but you've actually made a discourse on taxation interesting, accessible, and applicable. Thank you.

Great article! I broadly agree with this approach, but as a mom of a large family, I can't help but wonder: could this have the unintended effect of (effectively) taxing parents at a higher rate than non-parents? Those with kids are often forced to spend more of their money upfront (on education, gas, groceries, housing) and can't afford to save/invest as large a percentage of it. When we (and many of our friends) ceased to be DINKs and became parents, two immediate effects were:

1) Loss of gross income as one parent (typically mom) scaled back work hours or left her job to care for kids. This kicked many of us down to lower "income tax brackets";

2) More immediate, upfront "consumption spending" and less ability to save/invest. Those of us who had "saved aggressively" before kids could no longer sustain this, at all. This problem gets worse, not better, over time due to upfront costs of education, housing, transportation etc. that disproportionately affect larger families. I would consider this essential, rather than luxury consumption; most couples we knew, after having kids, were doing less luxury spending than before, but "consuming" more from their paychecks overall.

Even assuming no loss of income, this creates a situation where a couple might be penalized or stand to lose *relative* purchasing power if they chose to accept the upfront costs that come with children. I still think that consumption-based taxation is probably the best (and maybe inevitable) way forward, but I'd be curious about exemptions/mitigating incentives that could avoid further suppressing birthrate among the striver classes. Child tax credits, expanded childhood education savings accounts, school vouchers, housing/transportation tax relief for families, etc.