We Have To Do More To Lower GLP-1 Prices

Introducing new brand-name drugs isn't going to cut it

Today’s post is brought to you by my sponsor, Mechanize. They’re hiring junior software engineers at $300K/year base salary.

GLP-1 drugs are so effective at helping people safely lose weight that, if they were made widely available, the obesity rate could be pushed below 1980 levels in a single year. The issue is availability.

Retatrutide, CagriSema, Amycretin, Zenagamtide, Survodutide, MariTide, VK2735, Ribupatide, Berobenatide, Enicepatide, Elecoglipron, Pemvidutide and several other GLP-1-based drugs are all poised to enter the U.S. market within the next two years. If they all manage to make it through the FDA wringer, then there’ll be ten different companies pushing GLP-1 drugs, plus whoever else makes it through in that time. This is a dramatic juxtaposition with the current situation where the only competitors on the U.S. market are Eli Lilly and Novo Nordisk.

Competition improves products and lowers prices, benefitting consumers, right? Perhaps in theory, but in reality, these products are barely differentiated. The main factor setting any of them apart is how long doses last—a week or a month. But more importantly, I don’t think it’s likely that competition is going to meaningfully lower prices!

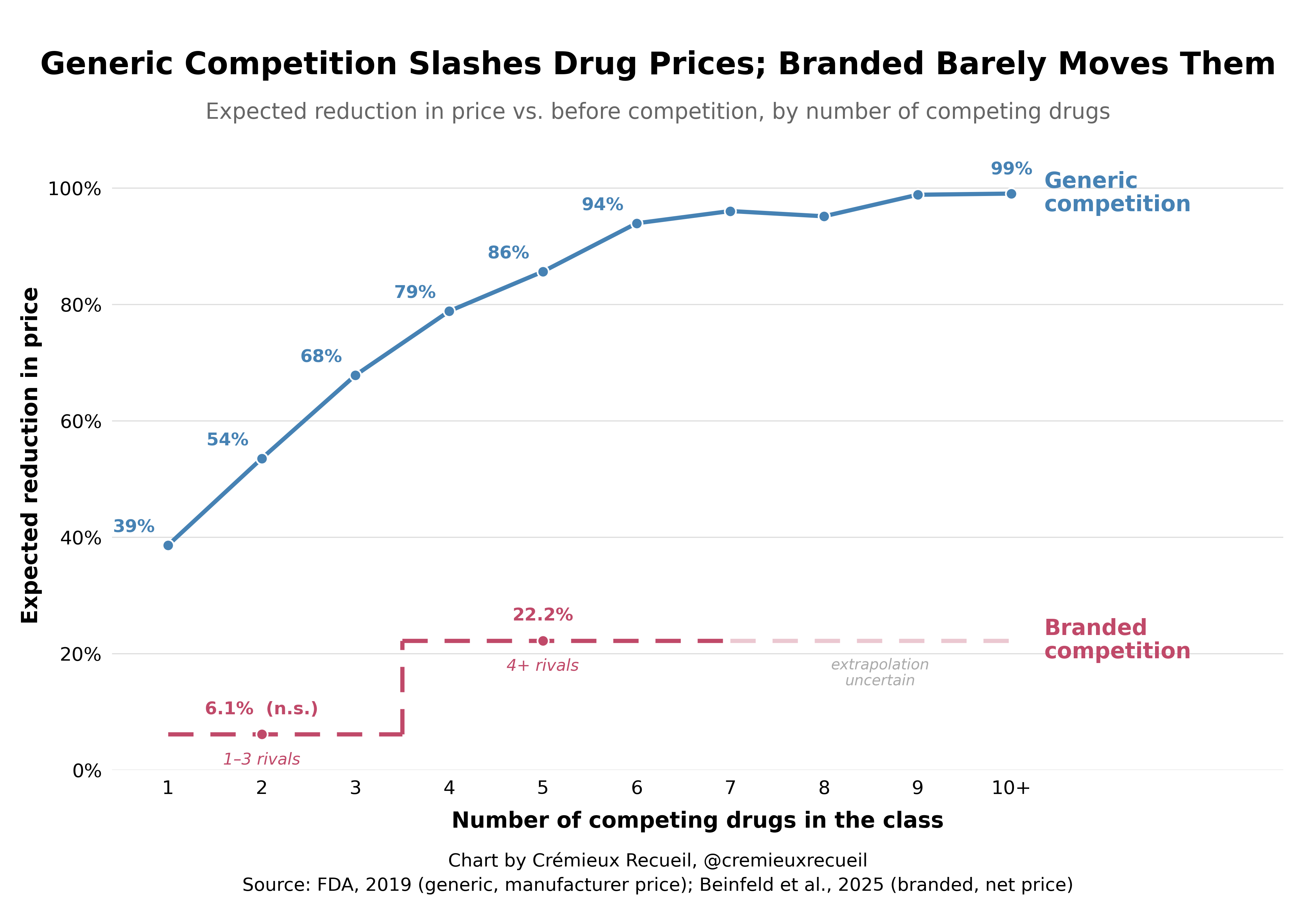

The general trend in medicine is for the introduction of new branded drugs to barely affect the prices of existing ones.1 The introduction of generic versions, on the other hand, leads to massive cost savings. Take a look:

The difference has to do with the fact that price competition only occurs when the buyer of the drug is treating the options available to them as interchangeable and the buyer is price-sensitive, with the ability to pick between options. By law, generics satisfy these requirements, but differentiated brands don’t necessarily satisfy any of them.2

With this in mind, what I expect from more GLP-1s is that the prices will remain exorbitantly high. They might go down a bit, but not so much that they’ll become affordable for average Americans or worthwhile for most health plans. That won’t happen until there’s a generic, and due to their abuse of the patent system, Novo Nordisk has managed to stall the entry of a generic in the U.S. by five whole years.

If we want to realize a world where America is skinny, we’ll have to figure something out. Unfortunately, there aren’t many viable options.

Use the Section 804 Importation Program. America has a program to import drugs from Canada, at the prices they’re sold at up there. This program needs reformed to be able to allow the mass importation of GLP-1s at Canadian generic prices, but it can be done. I’ve described how to do that, here.3 Meanwhile, this program can be used to at least match Canada on branded prices, which are quite a bit lower for them.

Protect Foreign Drug Import Optionality. The FDA has historically allowed people to bring in up to a 90-day supply of their prescriptions from abroad. They could, theoretically, allow people to import prescription drugs from a country with vastly lower prices like Brazil, India, or China, with the importing party being the one to take on all the risk. This is a very hands-off approach that’s unlikely to get much use, but it would allow some consumers to obtain licit, non-gray market, GMP drugs from other countries, at remarkably fair prices, with reasonable safety guarantees.

Protect Compounders. Compounding pharmacies have been the greatest force for getting down American GLP-1 prices to date. They’ve managed to deliver the drugs to millions of patients with almost no problems as a result. They’ve saved thousands of lives and billions of dollars. Novo Nordisk and Eli Lilly hate them for doing this, since they’ve undermined their sales. They’ve been trying non-stop to get the FDA to step in and stop the compounders from selling what is basically their drugs, for less. But the compounders are operating legally—if dubiously, and in the role of regulatory arbitrageurs—, and they should continue to be supported to keep prices low, so long as their quality remains sufficiently high.

Negotiate Down the Prices. The Inflation Reduction Act created a Medicare price negotiation program that has selected to negotiate down the price for the semaglutide products Ozempic, Rybelsus, and Wegovy. This takes effect on January 1, 2027 and constitutes a 71% discount from the list price for the CMS, meaning they’ll just pay $274 for a 30-day supply. This could be expanded on or pursued more aggressively.4

Protect the Gray Market. Gray market sales have allowed hundreds of thousands and perhaps millions to obtain very cheap GLP-1s without much issue. This option forces customers to take risks on their own and to do quasi-licit orders that might leave them scammed out of their money, but patients should be able to take these risks into their own hands. If this were a bigger thing, it could materially damage sales for branded drugs, but because patients are naturally averse to paying out-of-pocket, they want quality guarantees, and so on, it’s not a legitimate threat and it never will be. It’s also not worth thinking about in this case, since the branded drugmakers have extracted massively excessive profits by abusing America’s intellectual property laws.

How To Get Cheap Ozempic

If you want to skip the backstory and just get to the instructions, click here.

Buy Off a Patent. Congress could make an offer to one of the companies with an existing, approved GLP-1, paying them to give up their patent and allow generics into the market. This is unprecedented, but the authority is there, and if Congress wanted to make it happen, it could. It could do so at a relatively meager cost, too. Think about it:

What would happen to the value of, say, Novo Nordisk’s patent on semaglutide if the Presidential administration and the Congress pursued all of the options that I listed above? What if they also…

Put Medicare, Medicaid, ACA, FEHB, VA/DoD, and willing employer plans into a pooled purchasing process? This was done for hepatitis C drugs.

Made coverage expansion conditional on a low net price?

Attempted to tie public program prices to peer-country prices or to require rebates when prices exceed a benchmark level? They could even force manufacturers to rebate amounts above a benchmark price for drugs with a high budget impact.

Challenged improper Orange Book listings, limited 30-month-stay gamesmanship, and made it easier for follow-on versions to launch when core patents expired?

Authorized contract manufacturers to supply the government while paying the patent holder their “reasonable and entire” compensation per 28 U.S.C. §1498?

Let states pool GLP-1 purchasing and offer preferred placement in exchange for deeper supplemental rebates?

Force negotiated rebates to reduce what patients pay at pharmacies?

Required PBMs to pass through rebates and fees and choose drugs based on lowest net cost rather than on the basis of the largest retained rebate?

Prioritized review of follow-on GLP-1s, generic liraglutide and semaglutide pathways, alternative delivery forms, and competing incretins?

Paid full price only for patients who achieved agreed-upon outcomes like weight loss thresholds, A1c improvement amounts, low discontinuation, etc.?

Paid different net prices for diabetes, obesity, cardiovascular risk reduction, sleep apnea, MASLD, etc.?

Conditioned public coverage or preferred status on reliable supply, vial options, and transparent production?

Basically, the idea is to lower the margins associated with the on-patent drug the government wants to buy by as much as possible. Then, Congress could approach, say, Novo Nordisk with an offer that’s not just reasonable, but cheap given all the value low-cost GLP-1s would produce. This is possible, if only we have the will.5

This was a timed post. The way these work is that if it takes me more than one hour to complete the post, an applet that I made deletes everything I’ve written so far and I abandon the post. You can find my previous timed post here.

A message from my sponsor, Mechanize:

We’re hiring software engineers to build environments and evals that frontier AI labs use to train coding agents.

To get a better sense of the work we do, you can check out GBA Eval, where we had models build Game Boy Advance emulators from scratch and scored their performance.

Base pay starts at $300K/year for junior software engineers, with more for senior roles, plus equity and performance bonuses. Apply here.

This is drug at the list and net levels, but more so for list prices.

A generic is bioequivalent and AB-rated to a brand. Legally and clinically, it’s indistinguishable, and in some states, pharmacists must substitute the generic without calling the prescribing doctor to tell them. A ‘me-too’ brand, by comparison, is a different molecule, so they are not automatically substitutable and buyers can’t treat them as one commodity, so they fail to compete as one commodity. This is basically the difference between Bertrand competition and monopolistic competition.

In a branded drug class—meaning one without generics—, there’s an agency problem because the prescriber picks the drug, the patient pays a copay, and the insurer pays the balance but doesn’t make the prescribing choice. Thus, nobody is shopping on price and demand is price-inelastic, without any pressure to make cuts. A second branded option just gives prescribers another high-priced option. With a generic, on the other hand, the decisions moves towards the pharmacy or the PBM, which is price-sensitive, either capturing the spread on acquisition or having a payer mandate to do the lowest-cost dispensing.

A ‘me-too’ branded drug also holds its own patents and exclusivity, so it never has to compete on price because it competes on differentiation, opinion, and PBM rebates for formulary placement. Rebates help drugs to obtain position, and they frequently end up pocketed by middlemen. Generics only play a role when exclusivity has lapsed, and they don’t have marketing, so they can only compete on price, which they do. Thus:

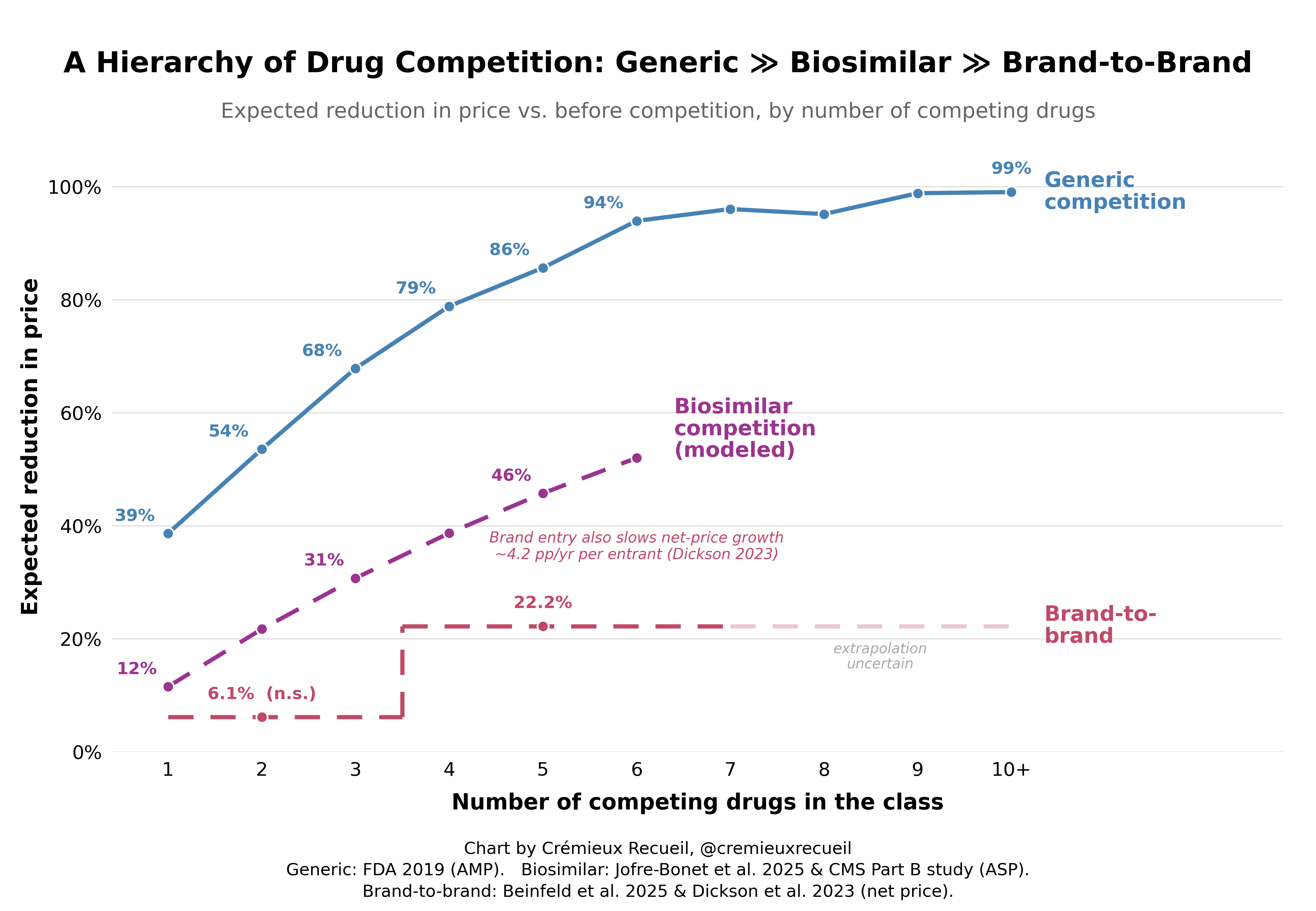

But note where competition does matter: it matters on the launch of new branded drugs. More branded drugs in a category means lower initial prices for the new ones.

We can also redo the earlier chart, as such:

Unfortunately, the cost-savings aren’t so low as if they were imported from, say, India or China, where the generic price reductions are free to go lower than they are in Canada.

Relatedly, the GLP-1 Bridge program is allowing Medicare Part D beneficiaries access GLP-1s for weight loss for a $50 copay between July 1, 2026 and December 31, 2027. The drugs are being supplied at a $245 net price per monthly supply in that time.

Unfortunately, many members of Congress would oppose this due to their personal funding and because they are opposed in principle, even when the company being pressed on would be a noted patent system abuser like Novo Nordisk or Eli Lilly.

Eliminate PBMs from the equation and branded drug prices fall.

All of this boils down to, “we should steal value from the company that developed the patent by force, having already told them to invest billions developing a drug in exchange for the patent.”

That’s not a good take. If anyone should get rich on this it’s the people who make these drugs.

If you think that the health benefits are high then you can lobby congress to buy out the patent or subsidize the cost. These debates literally happen. I’ve been in them. People present studies and argue that congress should allocate more resources.

The hard part is simply that congress does not believe that the health benefits are worth subsidizing the cost. They believe this based on studies that show as much. I’m skeptical of these studies long term, but they have been convincing to congress. They don’t want to cough up the funds.